Optimal Protocol Revenue Utilization

Some blockchain protocols generate revenue, and what they do with that revenue shapes their long-term trajectory and market viability in the eyes of economic participants. Historically, the "meta" in crypto has been some flavor of token buy-back-and-burn: use protocol profits to purchase the native token on the open market, then send those tokens to a burn address where they are permanently removed from circulation. The appeal is straightforward, as burning reduces circulating supply and should, in theory, translate into higher token prices if demand remains constant. In practice, these mechanisms have come under scrutiny as people recognize that markets do not necessarily respond cleanly to deflationary pressure, and that protocols could better reinvest that revenue to serve and grow the token ecosystem.

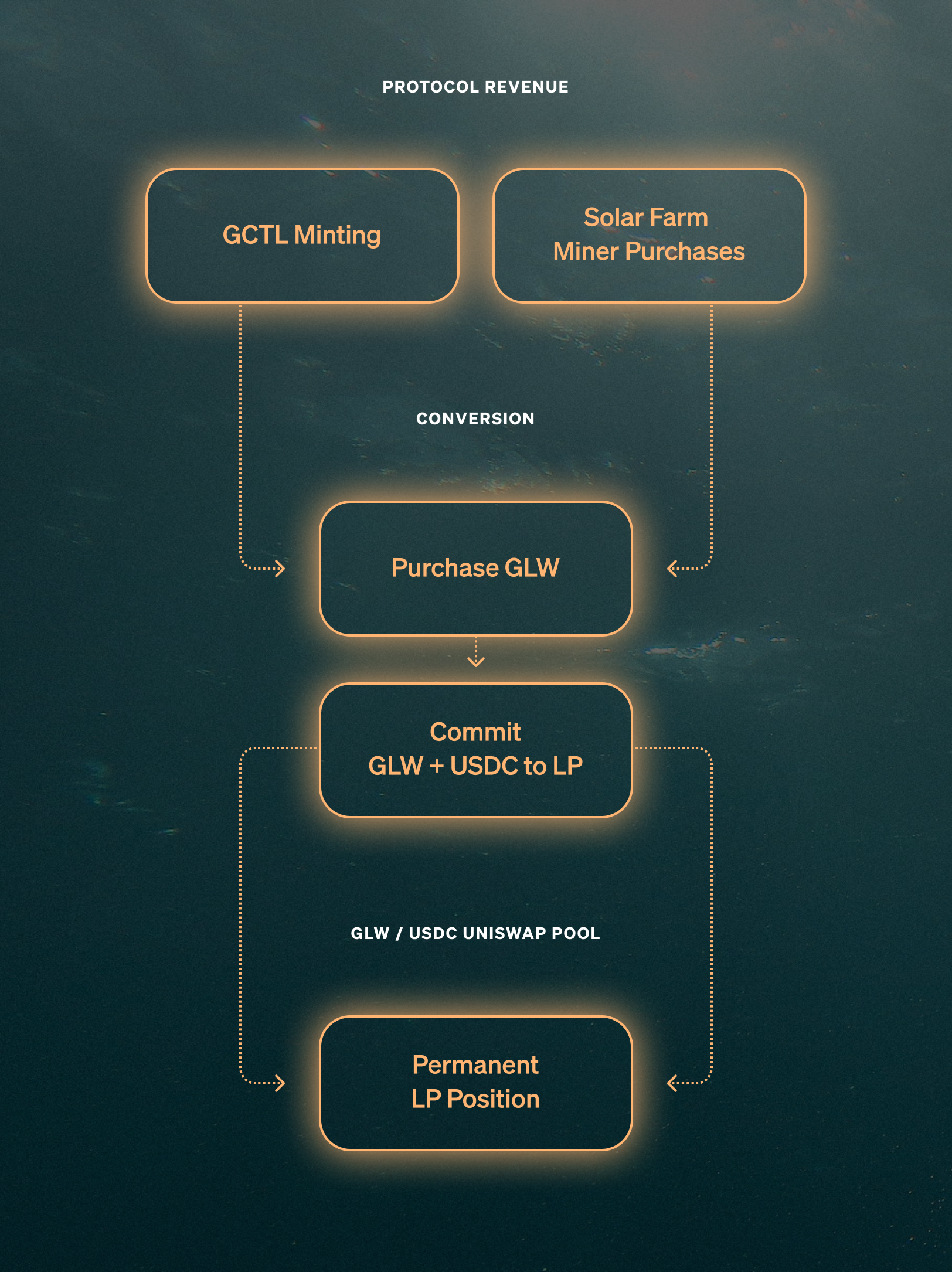

Glow implements embedded liquidity as an alternative to transient deflationary supply-side mechanics, where revenue becomes permanent liquidity infrastructure that indefinitely supports the ecosystem. When revenue enters the Glow protocol, primarily through GCTL minting by participants who want to direct regional solar construction subsidies, that capital flows into the Glow Endowment. The Endowment is Glow's embedded liquidity position in the GLW/USDC Uniswap pool: when revenue arrives as USDC, half of it is used to purchase GLW tokens, and the full amount, now split between GLW and USDC, is committed as liquidity to the pool. This commitment is a one-way transaction; once the liquidity enters the pool, it cannot be withdrawn.

Figure 1: Protocol revenue is used to purchase GLW, then committed alongside the remaining USDC as permanent liquidity to the GLW/USDC Uniswap pool.

The consequence of this design is that GLW tokens entering the Endowment are effectively removed from circulating supply, as they cannot be sold by the Endowment and can only be purchased out of the liquidity pool by someone swapping USDC for GLW. In this sense, embedded liquidity achieves the same "supply removal" that burning promises, but instead of destroying value, it creates utility. Unlike burning, this supply removal accelerates automatically during price declines: as GLW becomes cheaper, the Endowment's USDC reserves absorb more tokens without requiring any additional protocol revenue.

Understanding the Glow Endowment

Consider $10,000 of new revenue arriving from GCTL minting. The protocol uses $5,000 of it to purchase GLW tokens on the open market. The resulting GLW tokens, now worth $5,000, are paired with the remaining $5,000 of USDC and deposited together into the GLW/USDC Uniswap pool as a liquidity position. This is the Glow Endowment: a growing LP position owned by the protocol, committed permanently to providing liquidity for GLW trading.

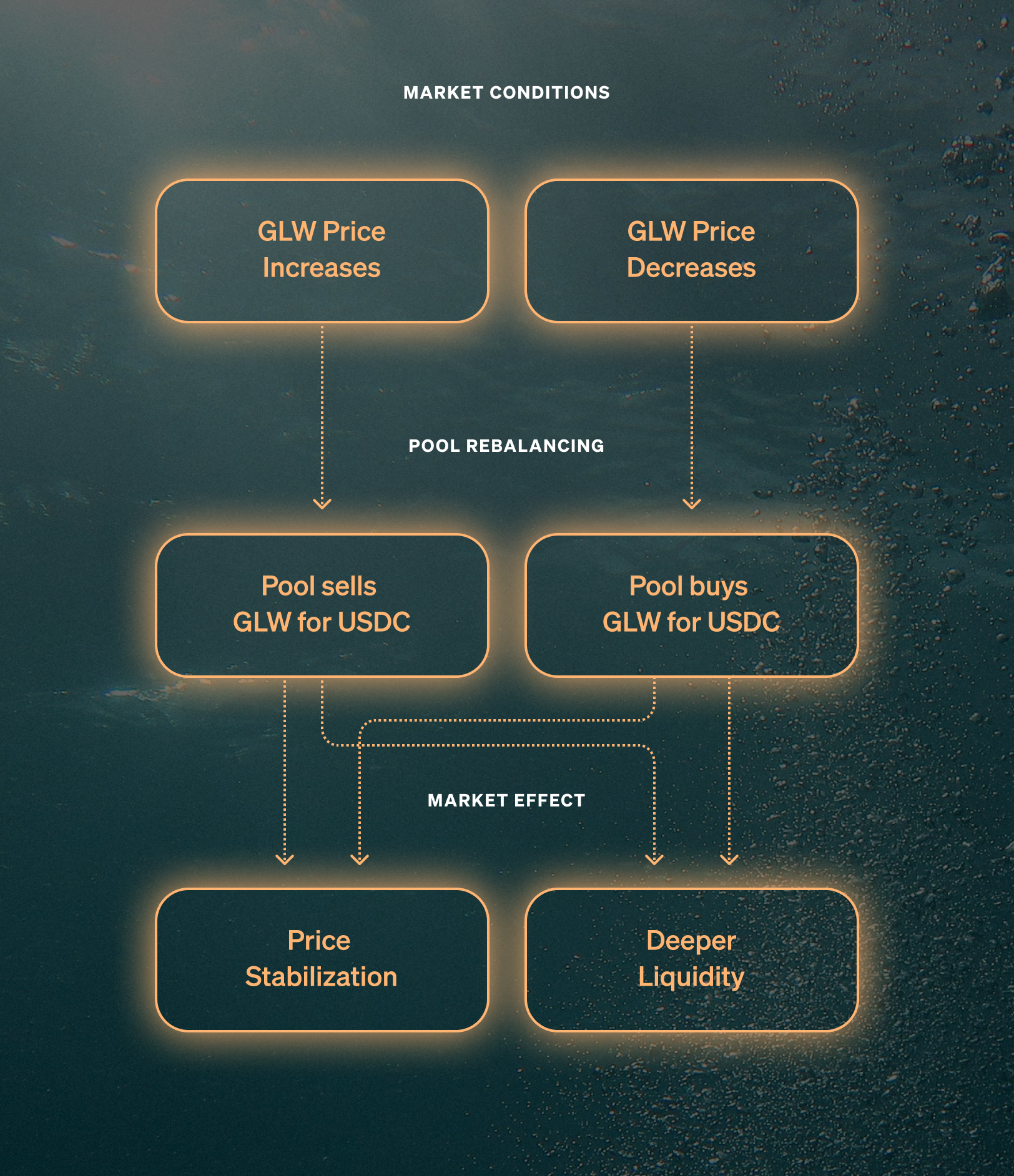

Because the Endowment is a Uniswap LP position, it naturally maintains a balanced portfolio of GLW and USDC. Uniswap v2 pools use a constant product formula that automatically rebalances LP positions to maintain equal dollar values of each asset. When GLW appreciates, the pool sells GLW and accumulates USDC; when GLW declines, the pool uses its USDC reserves to absorb GLW from circulation. This rebalancing happens automatically through trading activity against the pool as the Endowment continuously pulls GLW out of circulation during downturns without requiring any new capital inflows.

Figure 2: The Uniswap pool's constant product formula creates automatic rebalancing that stabilizes prices and deepens liquidity over time.

This rebalancing behavior means the Endowment automatically accumulates GLW when prices fall and reduces GLW exposure when prices rise, acting as a stabilizing force in the market that provides natural resistance to extreme price movements in either direction.

The primary source of Endowment inflows is GCTL minting. GCTL is Glow's control token that grants holders the ability to direct GLW subsidies toward specific infrastructure projects and regions, and when someone mints GCTL, typically because they want to steer subsidy dollars toward solar construction in a region they care about, the mint price flows directly into the Endowment. The mint price itself is calibrated to the square root of the GLW token price, so when GLW is worth $9, minting one GCTL costs approximately $3, and when GLW rises to $100, the mint price increases to $10. This creates a relationship where GCTL becomes more expensive to acquire as the underlying network grows in value, aligning the cost of control with the scale of the network.

Compounding Value Accrual

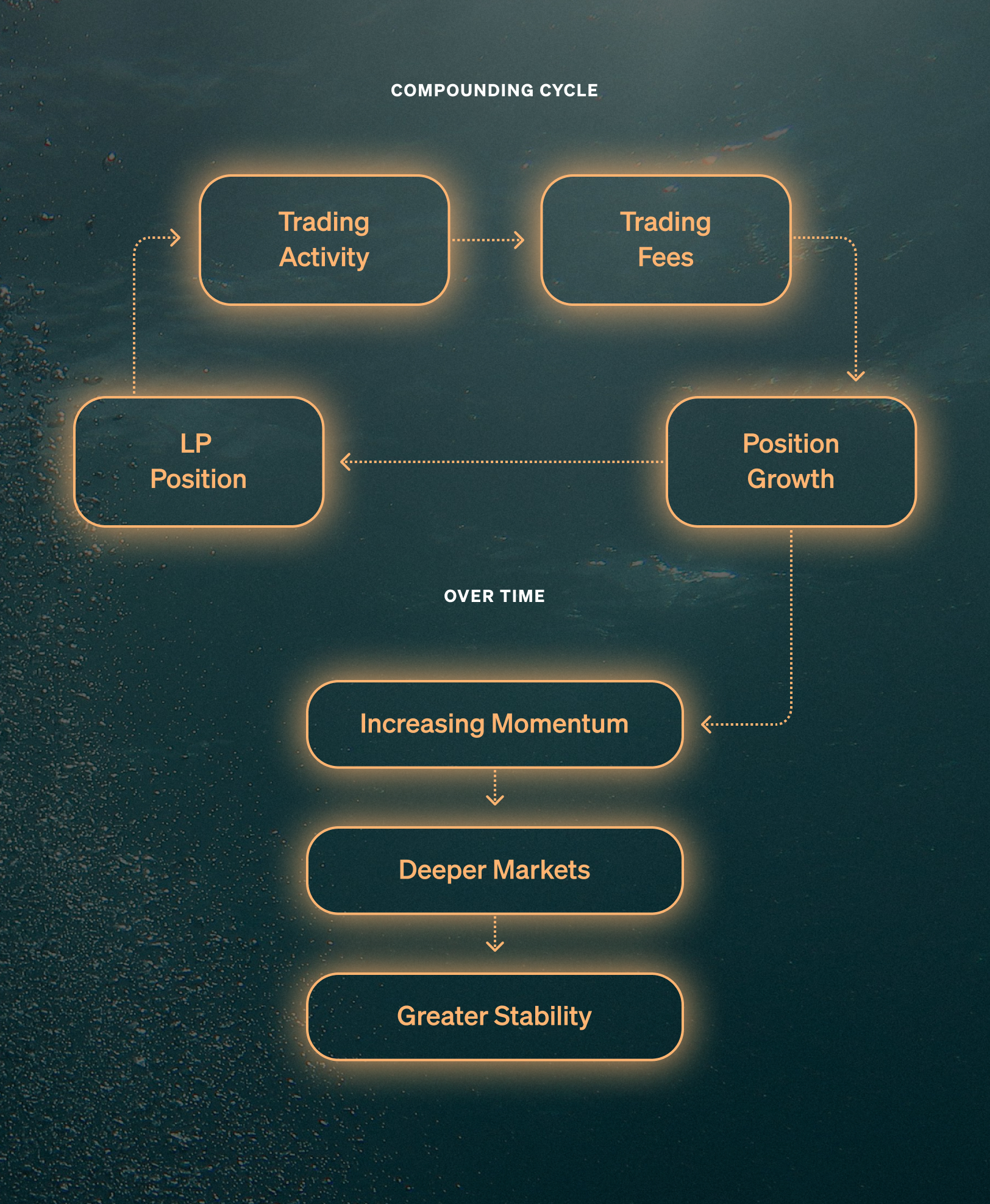

Embedded liquidity is inherently self-perpetuating. The Endowment's LP position earns trading fees on every swap, and those fees compound directly back into the position.

Every swap executed against the GLW/USDC pool generates a small fee, and the Endowment captures its proportional share based on its share of the total liquidity. These fees do not leave the system; they compound directly back into the Endowment's liquidity position. The result is a compelling gravitational quality to this mechanism. Liquidity begets liquidity: a larger pool earns more fees, and more fees mean faster growth. As the Endowment grows, its rate of accumulation accelerates because each additional dollar of liquidity pulls in more trading volume that generates more fees that add more mass. What begins as a small pool gradually becomes something with undeniable gravitational pull, attracting capital and activity simply by virtue of being deep and stable.

A small pool is fragile and easily moved by smaller market participants. A large pool is dense, absorbing shocks that would destabilize thinner markets. The longer the system runs, the more mass it accumulates. Greater mass brings both resilience and the capacity to serve larger financial actors.

Figure 3: Trading fees feed back into liquidity, creating self-reinforcing growth that accelerates over time.

Protocol revenue flows directly into a compounding public good. The Endowment benefits every GLW participant, and it grows stronger over time as fees accumulate on top of new contributions.

Building for Permanence

Deep liquidity is critical infrastructure for any token ecosystem. When liquidity is thin, large trades move prices dramatically: a solar farm looking to sell earned GLW tokens faces significant slippage if the pool cannot absorb the sale, and an investor looking to build a position pays a premium that scales with the size of their purchase. Thin liquidity creates friction that discourages participation and limits the scale at which the ecosystem can operate.

Deep liquidity solves these problems by allowing large trades to execute with minimal price impact, enabling new participants to enter at stable prices and existing holders to exit without cratering the market. The ecosystem operates with less friction, enabling larger-scale participation and more efficient price discovery. For Glow specifically, deep liquidity means solar farms can reliably convert their GLW rewards into operating capital and climate buyers can acquire large positions without excessive slippage. Investors can establish large positions without paying an entry premium or demanding higher returns to compensate for illiquidity risks. As a result, the token becomes a credible medium for the substantial capital flows that infrastructure deployment requires.

Embedded liquidity directly addresses this need by making every dollar of revenue increase the depth of the trading pool. The Endowment becomes a permanent market maker that will reliably absorb trading flows. As the Endowment grows, so does the ecosystem's capacity to handle larger participants and larger transactions.

Glow optimizes for permanence. Solar farms joining today benefit from liquidity built by participants years ago, and their participation builds liquidity that will serve participants years from now. The Endowment grows more valuable with age, continually compounding its way toward generating the deep, stable markets that large-scale clean energy deployment demands.